Gasoline prices continue to rise in the United States despite the temporary truce in the Middle East, with the $4-per-gallon level becoming a new norm. In several cities, drivers are paying as much as $5, while prices exceed $6 in states such as California.

Detail

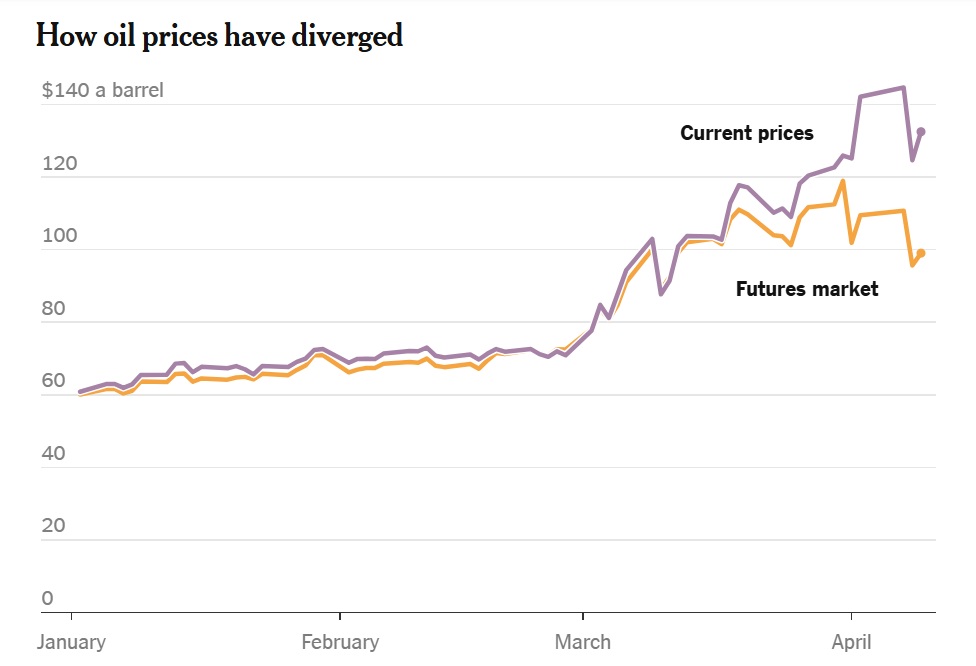

Despite the decline in oil futures prices, the physical market remains under strong pressure. Disruptions to oil flows through the Strait of Hormuz have kept supply constrained, forcing refiners to pay higher prices to secure spot shipments.

Spot oil prices have reached around $145 per barrel in some trades, compared to much lower levels in futures contracts. This gap means fuel production costs remain elevated, directly impacting consumers.

Futures prices have also rebounded toward $98 per barrel, signaling continued market tension. Analysts say gasoline prices would require oil to stay below the mid-$90 range to ease, a scenario that is currently unlikely.

In contrast, prices do not fall as quickly as they rise. Gas stations tend to reduce prices gradually after shocks, first working through higher-cost inventories, which slows the pass-through of declines to consumers.

Geographically, states such as Hawaii, Idaho, and Utah have been among the most affected by recent increases, while California has recorded record levels, particularly in diesel.

Economically, the burden on consumers and businesses is mounting, with estimates suggesting a total impact of up to $100 billion if current prices persist through the end of the year, according to JPMorgan estimates.

What’s next?

Price trends will depend on the resumption of oil flows through the Strait of Hormuz and stabilization in the physical market, with attention on whether any decline will reach consumers or remain delayed.